👀Zhipu AI and MiniMax Just Went Public, But They're Not China's OpenAI

Despite their research pedigrees and frontier AI ambitions, both companies’ business models reveal uncomfortable truths about operating AI startups in China.

When Zhipu AI and MiniMax, two leading Chinese AI and LLM startups, went public on the Hong Kong Stock Exchange this week, headlines enthusiastically crowned them as “the world’s first publicly-traded LLM companies” and “China’s OpenAI.”

Their stock prices rose on debut: Beijing-based Zhipu AI, founded by Tsinghua University researchers, rose 13% on Thursday after a $558 million IPO, making it the first major Chinese LLM startup to go public.

Shanghai-based MiniMax, founded by former SenseTime executives, raised HK$4.8 billion ($620 million) in its IPO, doubled on its first day of trading in Hong Kong on Friday.

Their IPO validated years of work building LLMs in one of the world’s most competitive AI markets. As China’s 2nd generation AI startups, following the computer vision-focused 1st generation of SenseTime and Megvii, Zhipu AI and MiniMax were fortunate in their timing.

Founded in 2019 and 2021 respectively, they rode the wave of the Transformer architecture, GPT models, and diffusion techniques—technologies far more generalizable than CNN-led computer vision and applicable to vastly larger market opportunities.

They are undoubtedly beneficiaries of OpenAI’s market education; without ChatGPT’s explosive demonstration of LLM capabilities in late 2022, neither company would command their current multibillion-dollar valuations.

Despite vastly different founding stories and business approaches, both have been labeled China’s answer to OpenAI. But they are not China’s OpenAI. Look closer at their business models, revenue structures, and strategic choices, and a different picture emerges—one of constant compromise, survival-mode pivoting, and the fundamental structural differences between China’s AI ecosystem and Silicon Valley’s patient capital environment.

Two Different Origins

Zhipu AI emerged as a classic academic spinoff. Founded in 2019 by Tsinghua University computer science professors Tang Jie and Li Juanzi, the company grew directly out of Tsinghua’s Knowledge Engineering Group (KEG). It initially focused on knowledge graph before quickly pivoting to LLMs.

Just one year after Zhipu’s founding, OpenAI released GPT-3. The company responded by introducing their own LLM called GLM in 2021, followed by GLM-130B in 2022. While they struggled to convince Chinese venture capitalists about the potential of LLMs during early fundraising, OpenAI’s ChatGPT launch in November 2022 shifted the landscape overnight. Suddenly, Zhipu AI—one of the few Chinese startups already developing LLMs—became highly sought-after.

The company’s mastermind is Tang Jie, the co-founder and chief scientist. He was one of the technical leads in BAAI’s Wudao project, China’s Manhattan Project-style first LLM experiment, and helped nurture talents who went on to develop LLMs elsewhere, including Yang Zhilin at Moonshot AI.

The funding followed quickly. By October 2023, the company secured a massive 2.5 billion RMB (~$350 million) investment led by Alibaba and Tencent. In May 2024, Saudi Arabia’s Prosperity7 Ventures joined a $400 million round, valuing Zhipu at around $3 billion.

Throughout 2023 and 2024, Zhipu released ChatGLM-6B, a 6-billion-parameter conversational model, and expanded its model lineup with GLM-V (a vision-language model), Ying (a Sora-like video generator), and AutoGLM (a GUI agent). Their latest GLM-4.7 now ranks among the smartest open-weight models globally.

In the meantime, Zhipu accelerated its global expansion by providing on-premise AI solutions, bundled as “AI-in-a-Box” servers to governments and enterprises in regions such as Southeast Asia and the Middle East. However, starting in 2025, the company has been added to the U.S. Department of Commerce’s Entity List (trade blacklist), amid U.S. concerns over Chinese AI firms and national security.

MiniMax followed a different path. CEO Yan Junjie, a former Vice President at SenseTime with an over 30,000 citations, founded the company in 2021 with two partners, all from SenseTime. The startup’s name derives from the minimax algorithm, which searches for optimal solutions in worst-case scenarios.

MiniMax’s mission is “Intelligence with Everyone” and their first product, Glow, allowed users to create virtual AI characters with custom backstories and personalities for open-ended conversation. The app proved successful, amassing nearly 5 million users within four months before being suspended in mainland China due to lacking required government registrations.

This unexpected consumer success pushed MiniMax in a direction quite different from Zhipu’s enterprise focus. At one time the company maintained more product managers than researchers.

Forced to pivot by regulatory issues, MiniMax redeployed Glow’s concept as Talkie, an English-language AI companion app targeting overseas markets. The move paid off quickly: by June 2024, Talkie ranked as the 5th most-downloaded free entertainment app in the U.S. and surpassed Character.AI to become the No.1 AI companion app in downloads. More than half of Talkie’s users were American, contributing to 11 million monthly active users worldwide by mid-2024.

In September 2024, MiniMax entered generative video with Hailuo Video-01, a text-to-video model. The company didn’t release a frontier LLM until January 2025 with MiniMax-01, later followed by reasoning models M1 and M2 that claimed top positions among open-weight models. MiniMax also demonstrated strength in speech synthesis, releasing Speech-02 in April 2025.

The Business Model Problem: Old Wine in New Bottles

Despite their research pedigrees and frontier AI ambitions, both companies’ business models reveal uncomfortable truths about operating AI startups in China.

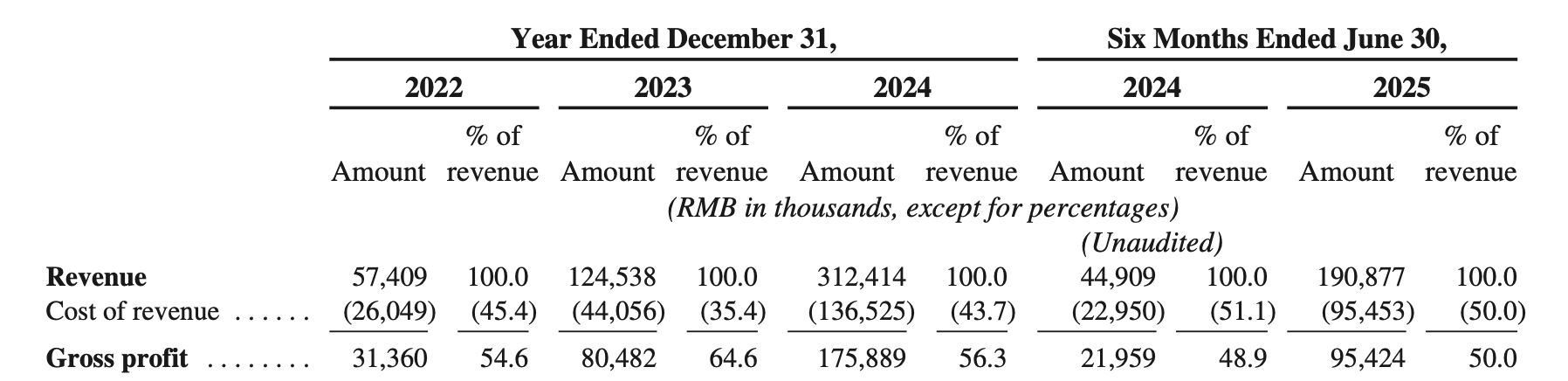

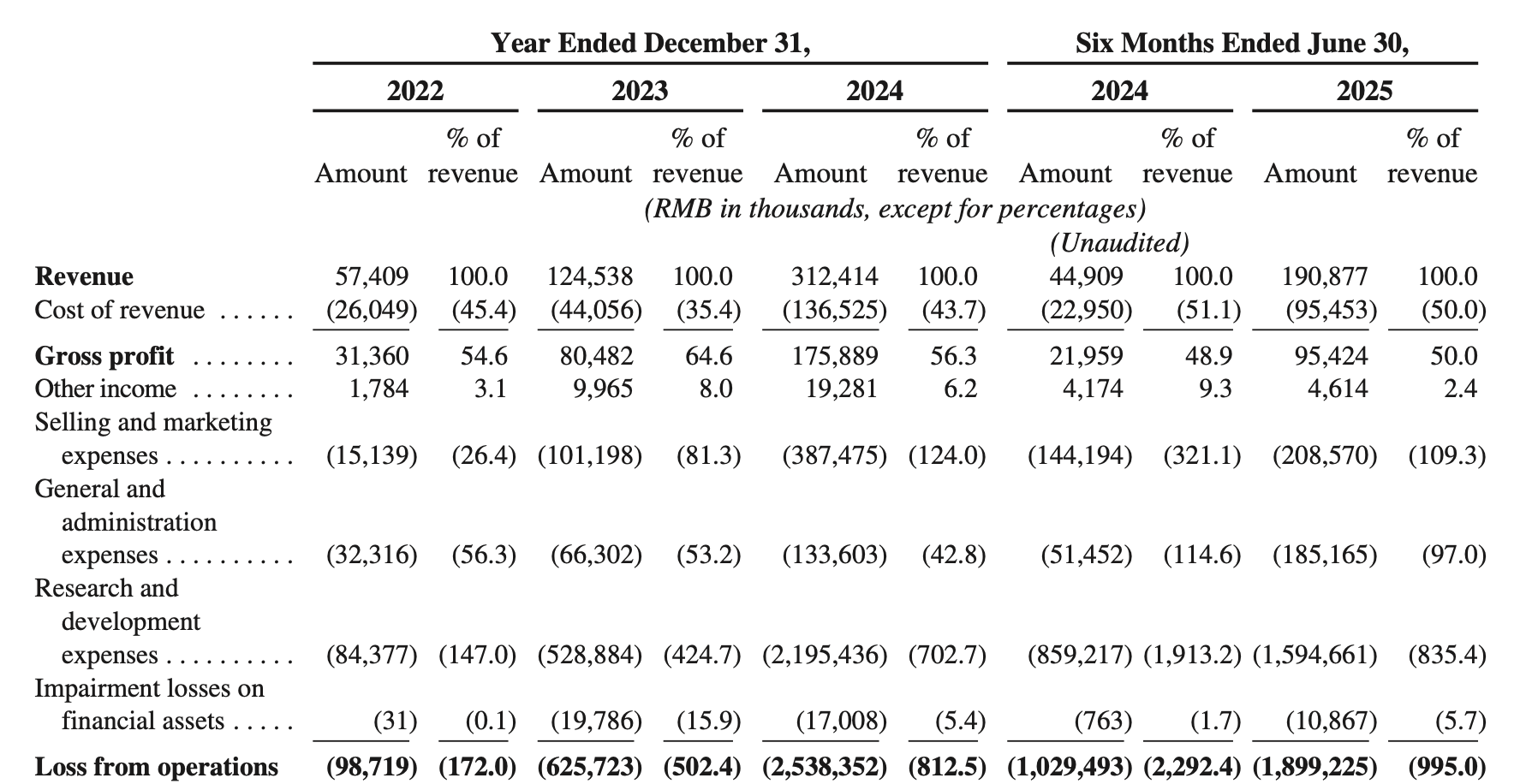

Zhipu AI’s revenue trajectory looks impressive on paper: from 57.4 million RMB in 2022 to 124.5 million in 2023, reaching 312.4 million (~$44.8 million) in 2024, an annual compound growth rate of 130%.

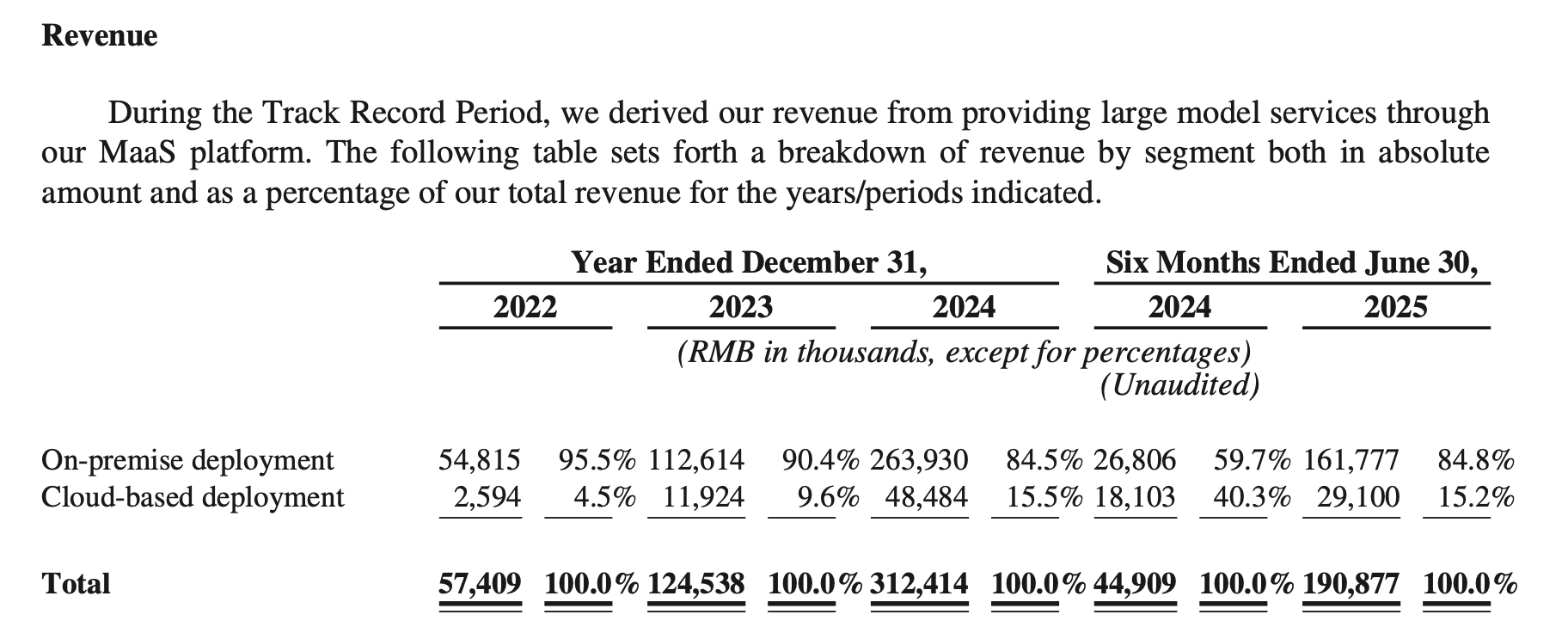

About 85% of Zhipu’s 2024 revenue came from on-premise deployment, which is essentially project-based services for governments and enterprise clients who are more sensitive to data privacy. While this business achieved a 66% gross margin in 2024, it represents precisely the kind of project-heavy model that characterized Chinese AI 1.0 companies like SenseTime and prevented them from scaling rapidly. These deployments often involve long payment cycles, and significant customization work.

Zhipu recognized this limitation and has been expanding its model-as-a-service API business. But their cloud API segment represents only 15% of 2024 revenue and operates at a razor-thin 3.4% gross margin, squeezed by China’s brutal API pricing war. By the first half of 2025, this margin had turned negative at -0.4%.

As an LLM startup, Zhipu’s R&D spending is staggering: nearly 2.2 billion RMB ($315.3 million) in 2024, representing 703% of revenue. Approximately 70% of that R&D budget goes directly to computing power.

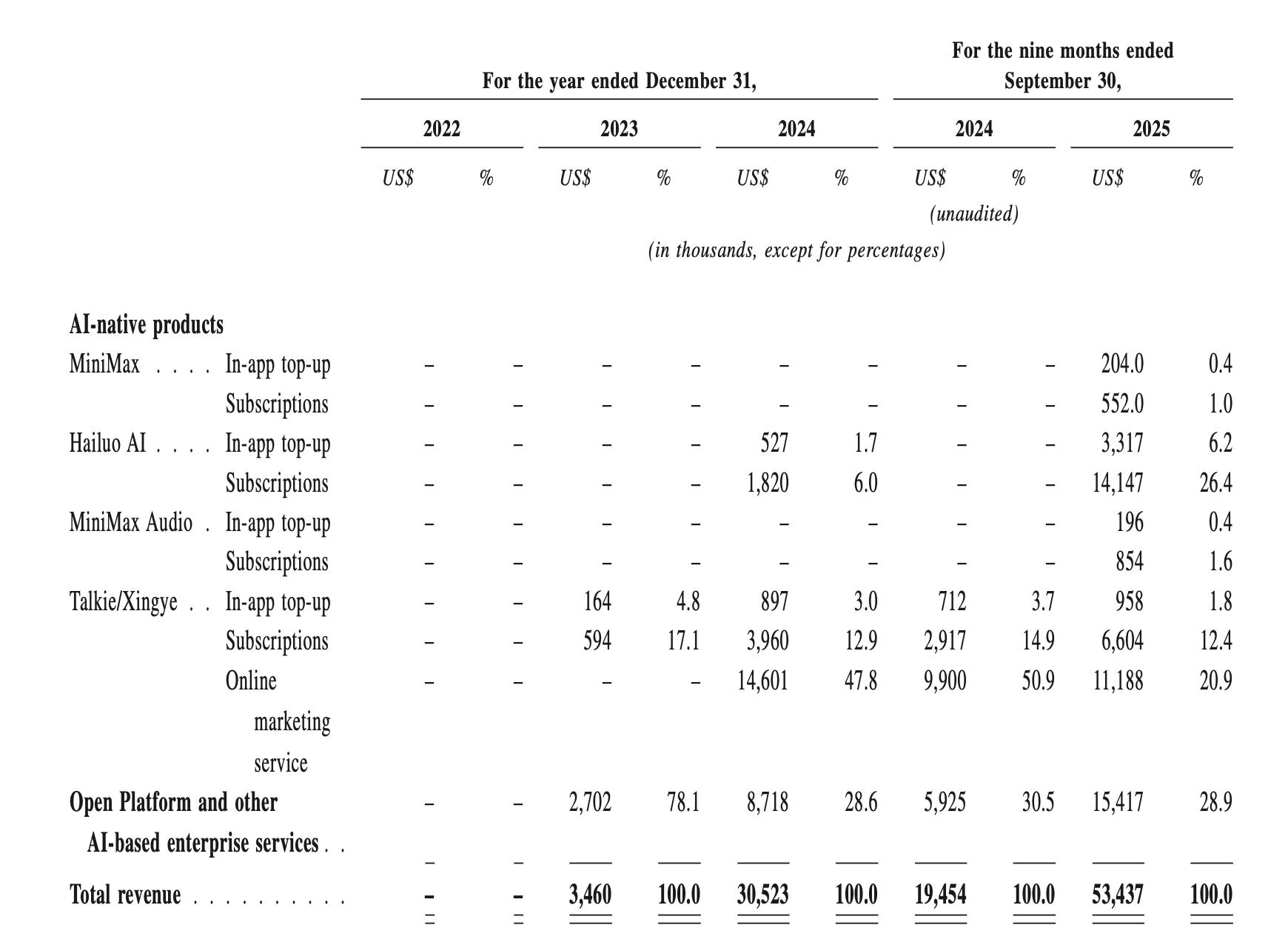

MiniMax’s revenue grew from approximately $3.5 million in 2023 to $30.5 million in 2024, reaching $53.4 million in the first nine months of 2025, with an overall gross margin of 23.3%. Unlike Zhipu’s mainland China focus, MiniMax derives roughly 70% of revenue from overseas markets, particularly the U.S. and Southeast Asia. These figures also mask profound losses: $465 million in 2024 and a staggering $512 million in the first nine months of 2025 alone.

MiniMax operates more like an AI application company than an R&D-driven research lab. The two AI consumer apps (Talkie and related products) contributed $38 million of revenue in the first nine months of 2025, but AI companion apps face increasing regulatory scrutiny globally, with concerns about soft pornographic content, mental health implications, and parasocial relationships.

While MiniMax’s B2B business, Open Platform and Other Enterprise Services, represents a declining share of total revenue, it achieved a remarkable 69.4% gross margin in the first nine months of 2025, far exceeding industry averages. This suggests MiniMax has achieved significant advantages in model inference cost control.

The Luxury of Patient Capital

Neither Zhipu AI nor MiniMax has had the luxury that OpenAI enjoyed, the ability to pursue frontier research for years without immediate commercial pressure.

OpenAI operated for nearly seven years before releasing a commercially viable product. Founded in 2015, the company could focus purely on research through 2022, burning through hundreds of millions in compute costs and staff wages while publishing groundbreaking papers and training increasingly large models. When GPT-3 launched in 2020, OpenAI had already established technical leadership. ChatGPT’s release in late 2022 then created a commercial tsunami that justified all those years of patient investment.

Zhipu AI and MiniMax never had this option. In China’s venture capital environment, investors expect quicker returns and clearer paths to profitability. The companies couldn’t afford to operate at massive losses for five to seven years while pursuing unproved, uncertain research directions. They needed to demonstrate commercial traction, show revenue growth, and prove their research could translate into paying customers, all while trying to advance the frontier of AI capabilities.

Both companies have been caught in a paradox: to survive and raise funding, they needed to show commercial progress, but the commercial activities distracted from the research breakthroughs that could create truly transformative value.

For example, between 2023 and 2024, Zhipu became one of the most aggressive investors in the Chinese AI market, acquiring or investing in eight AI companies over seven months. This diversification strategy suggests a company uncertain about its core direction, hedging bets across multiple AI companies rather than maintaining laser focus on foundational model excellence.

MiniMax approached the problem differently. They expanded marketing and advertising budgets in 2024 on promoting consumer applications that could generate revenue and user growth while building underlying models, two entirely different paths requiring different talent, different strategies, and different capital allocation decisions.

As a result, 2024 was a year of strategic confusion for MiniMax. The company pursued everything from LLMs to text-to-speech to video generation to AI companions, trying to maintain revenue and user growth while also investing in foundational model development. As they focused on consumer apps, they inevitably faced fierce competition from tech behemoths like ByteDance and worried they couldn’t win that battle.

Late Awakening

Perhaps the most revealing irony is, despite being founded earlier with explicit missions to pursue general intelligence, Zhipu AI and MiniMax’s actual contributions to advancing AI have been no greater than labs founded much more recently.

DeepSeek, founded in 2023—years after both companies—has made arguably more significant contributions to the AI research community. Backed by High-Flyer, a quantitative trading firm with deep pockets and no need for near-term commercialization, DeepSeek could focus purely on research. DeepSeek-V3 and R1’s efficient training approaches, architectural innovations, and open release of frontier-capable models demonstrated what’s possible when a team can focus purely on research excellence without commercial compromise. The global recognition and explosive user growth that followed were inevitable byproducts of this technical progress.

Similarly, the AI research labs within Alibaba and ByteDance, Qwen and Seed, while part of larger corporations, operate with resources and focus that allow them to push frontiers more effectively than independent startups juggling commercial survival.

Throughout 2024, as Zhipu and MiniMax were caught between enterprise sales and consumer apps, these better-resourced labs were making steady progress on frontier LLMs.

After DeepSeek’s wake-up call in early 2025, both Zhipu and MiniMax shifted resources dramatically toward LLM development. Their models began alternating positions on benchmark leaderboards, and both companies accelerated development of agentic, coding, and reasoning capabilities. They finally started behaving like the frontier AI labs they had always claimed to be.

Tang Jie stated in an internal letter to Zhipu employees that by 2026, the company aims to achieve global leadership in large models, launch the next-generation model GLM-5, innovate new model architectures and scaling paradigms, and expand research into reinforcement learning and generalization.

If they could do this in 2025, why hadn’t they been doing it all along? The obvious reason is they couldn’t afford to, not in China’s commercial environment, not without the patient capital and institutional support that allows pure research labs to operate.

This isn’t a criticism of Chinese investors’ sophistication or risk appetite. Rather, it reflects different market structures, different regulatory environments, and different expectations about how technology companies should develop. But it does mean that an independent startup pursuing AGI faces much steeper odds in China than in the U.S.

Yet there’s a deeper, beneath the surface question: Do Zhipu AI and MiniMax truly believe in AGI? OpenAI was founded by people who genuinely believed AGI was achievable and worth pursuing at any cost. DeepSeek’s singular focus on pushing model capabilities suggests similar conviction. But do Zhipu and MiniMax share this almost religious commitment to AGI, or are they just primarily excellent AI companies?

When Liang Wenfeng started his company (DeepSeek) in 2023, we had a conversation. At the time, I didn’t realize how committed he was to AGI—I’m grateful for the different perspectives he brought me. Choosing to persistently pursue AGI technology, continuously exploring the upper bounds of AGI, while making precise predictions about the future—these are areas where Zhipu needs to keep improving and elevating itself going forward.

—Tang Jie

None of this is to diminish what Zhipu AI and MiniMax have accomplished. Both companies have built impressive technical capabilities, created valuable products, and navigated an extraordinarily complex and competitive market. Their public listings represent meaningful validation and provide capital for continued development.

But calling them “China’s OpenAI” fundamentally misunderstands what OpenAI was and is: a research lab that could pursue original, breakthrough technologies for years without commercial pressure, a group of people who irrationally believe AGI.

The question for 2026 and beyond is whether Zhipu and MiniMax’s recent pivot toward intensive LLM development represents a sustainable new direction or merely another oscillation in their ongoing struggle to balance survival and frontier research. Their public listings provide new capital and visibility, but also new pressures to demonstrate returns. Whether they can finally escape the paradox that has constrained them from the start remains to be seen.

The -0.4% gross margin on Zhipu's cloud API segment says everything. They're losing money on every API call. When they hiked prices to $56, the backlash was instant but honestly they were just doing survival maths. Same with MiniMax bleeding $512 million in nine months. These aren't sustainable businesses at current pricing. They're market capture plays. Covered why the cheap providers should worry you more than the expensive ones: https://sulat.com/p/the-real-cost-of-cheap-ai-inference