💸Chinese AI Companies Just Had Their Payday

DeepSeek, Moonshot, and StepFun are raising billions.

Chinese AI companies just had their payday over the past week.

DeepSeek, the Chinese AI lab backed by quant trading giant HighFlyer that just released its latest LLM V4, is reportedly seeking its first-ever outside funding. They initially targeted $300 million at a $10 billion valuation, but investors’ demand were insatiable. The round has reportedly climbed to $7 billion at a $50 billion—if successful, this will be the largest single funding for a Chinese AI company in recent history.

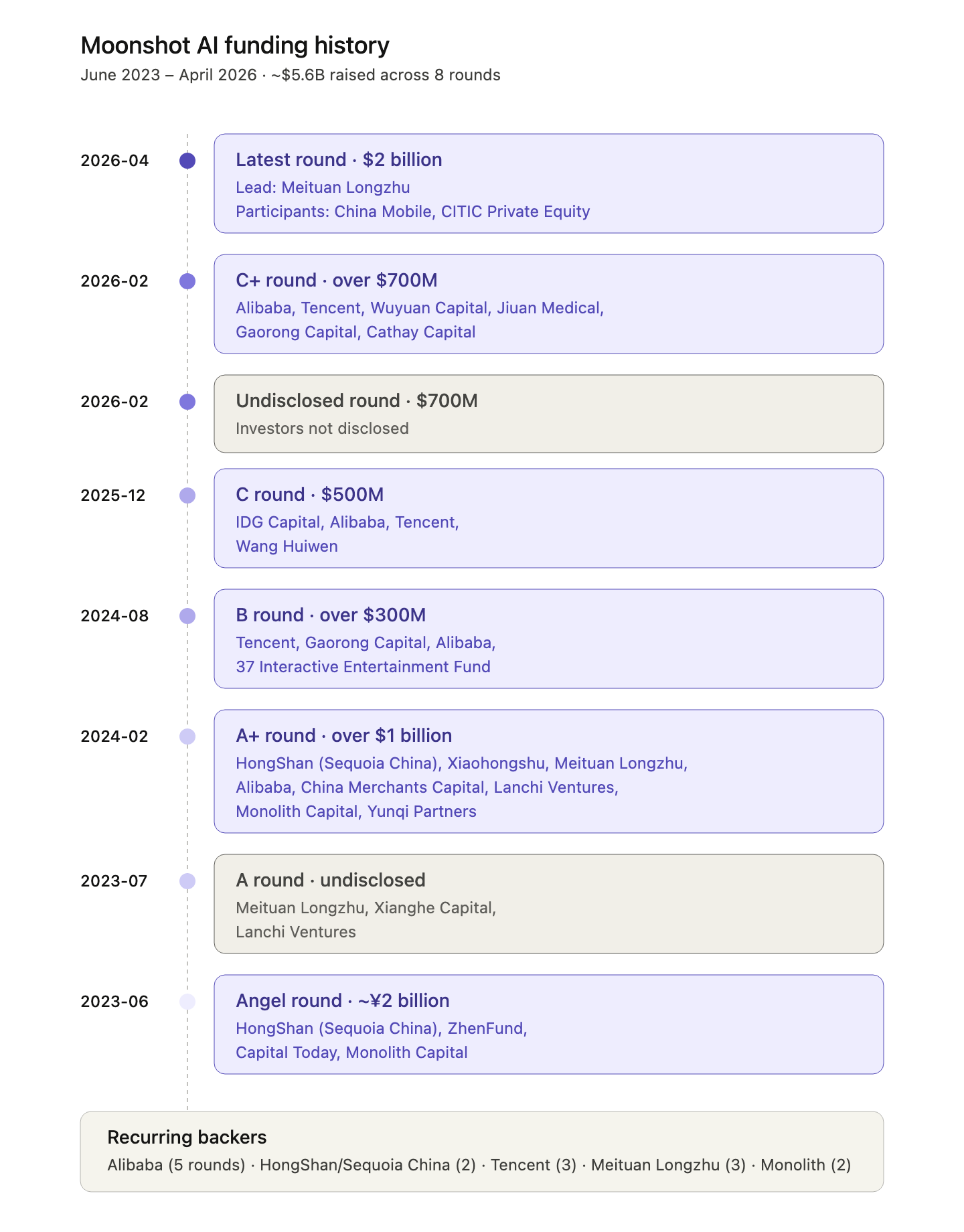

Then it’s Moonshot AI, the developer of the Kimi model family, just raised $2 billion at a valuation of over $20 billion, led by Chinese delivery giant Meituan. This is the third round of their fundraising this year, totaling $3.9 billion in six months, according to Chinese media outlet LatePost.

Finally, StepFun, a Shanghai-headquartered AI company and developer of the Step model series, reportedly close to raising $2.5 billion. Its valuation target was $10 billion months ago.

To put that in context: the last time a Chinese private company raised $2 billion-plus in a single round was Shein in May 2023, at a cut valuation of $64 billion, down a third from its prior round. From roughly 2021 to 2025, China’s tech VC market was in prolonged contraction—regulatory crackdowns against technology companies, US-China tensions, rising exit difficulties, global rate hikes. Therefore the recent fundings signal something has shifted.

Still, the numbers are overshadowed by their Western counterparts. OpenAI closed a record $122 billion round, valuing it at $852 billion. Anthropic raised $30 billion in February at $380 billion, and is now in talks for a new round at a reported $900 billion valuation—which would put it ahead of OpenAI.

But the gap is less important than the trajectory. Chinese AI companies have figured out their commercialization story in the agentic era, and investors are fear missing out.

DeepSeek

DeepSeek, founded in mid-2023, has never raised a single dollar before. Its backer, HighFlyer, is one of China’s largest quant trading firms, overseeing more than 70 billion yuan ($10 billion) with an average fund return of 56.6%, according to Bloomberg. That’s why DeepSeek could focus on research, commit to an open-source strategy, and ignore the pressure to commercialize or ship products on someone else’s timeline. Even after R1—its blockbuster reasoning model that made a global splash in early 2025—the company reportedly rejected funding offers from both Chinese and US investors.

What changed was talent retention. Competitors began aggressively poaching DeepSeek’s engineers and researchers. Luo Fuli, one of the DeepSeek V3 contributors, is now Xiaomi’s head of LLM team. Guo Daya, a core author of both DeepSeek V3 and R1, has joined ByteDance’s Seed lab. Without outside funding and a formal company valuation, researchers have no equity incentive, raising the cost of keeping the people who built the models.

There’s also a scale problem. V4 is nearly twice the size of V3, and the data used to train scales accordingly. DeepSeek is also allocating GPU resources toward unexplored research areas that require significant capital. Research at the frontier isn’t cheap, even for a company backed by a quant trading giant.

In April, DeepSeek reportedly started its first external funding round at a $10 billion valuation, seeking $300 million. Then China’s Big Fund—the state-backed semiconductor investment vehicle that also backs SMIC—is now in talks to lead the round at a $45 billion valuation, according to the Financial Times. Tencent is also said to be in discussions. The latest reporting from The Information is CEO Liang Wenfeng will personally invest 20 billion yuan ($3 billion), around 40% of the total amount, at a $50 billion valuation. DeepSeek is also expected to release V4.1 in June.

Moonshot AI

The Moonshot funding story was first broken by LatePost that the company was close to completing a new $2 billion round led by Meituan’s investment fund Longzhu, with China Mobile and CPE (previously known as CITIC Private Equity) also participating. LatePost also reported that Moonshot raised $1.9 billion across January and February, making the total $3.9 billion over six months (please note that the undisclosed round in February 2026 below was reported by LatePost; no other sources have surfaced details.)

According to Meituan Longzhu’s general partner, Moonshot’s annual recurring revenue (ARR)—mostly API revenue—reached $200 million in April. For comparison, Cursor’s ARR has surpassed $2 billion as of March 2026, and Cursor is in talks to raise $2 billion at a $50 billion valuation. Moonshot isn’t cheap at $20 billion, but it’s just starting to grow. And notably, Cursor’s models are in part trained on top of Kimi K series. Meanwhile, MiniMax and Zhipu, which both listed on the Hong Kong stock market, are valued between $35 to $70 billion. Against that backdrop, Moonshot at $20 billion looks like a discount.

Moonshot’s latest model, Kimi K2.6, is one of the best open-weight models available today. The trillion-parameter model features strong coding capability, long-horizon execution, and can handle up to 300 sub-agents simultaneously. A bigger and more powerful K3 is reportedly in development for later this year.

While Moonshot’s largest external shareholder should be Alibaba, which owns approximately 36% of the company after making its bet in early 2024, the fact that Meituan—currently locked in a fierce delivery war against Alibaba and JD.com—is Moonshot’s lead investor of this funding round signals an escalating AI arms race between China’s tech giants.

AI agents that order food and book hotel tickets are increasingly becoming the interface through which young people manage daily life. Alibaba is building its ecosystem around Qwen as the central agent for daily tasks. Meituan doesn’t want to be left behind. Moonshot’s coding and agentic specialization makes it a natural fit, from distribution via Kimi's consumer reach to agentic models powering Meituan's merchant and logistics ecosystem.

Meituan is also building its own AI models in-house. Its Longcat 2.0 model is reportedly trained on 50,000 to 60,000 Huawei Ascend chips—the largest training run on domestic Chinese compute infrastructure to date.

StepFun

Just one day after the Moonshot news, Shanghai-based StepFun was reported to be close to raising $2.5 billion.

For readers less familiar with the company: StepFun is one of the top five LLM startups in China, alongside DeepSeek, Zhipu, MiniMax, and Moonshot. Founded in April 2023 by former Microsoft corporate VP Jiang Daxin, its core team includes Zhang Xiangyu—former director of research at Megvii and co-author of ResNet, one of the foundational papers in modern computer vision—alongside other researchers from Microsoft Research Asia.

Their latest flagship model is Step-3: 321 billion total parameters, 38 billion active, with two architectural innovations that reduce KV-cache demands to roughly 22% of DeepSeek V3’s per-token cost. But language is just one dimension. StepFun has shipped 16 multimodal models—covering text-to-video, voice interaction, image understanding, and multimodal reasoning. The Step-Video-T2V model, co-released with Geely Auto in early 2025, was the largest open-source video generation model in the world by parameter count at the time of release.

The low-profile company made headlines earlier this year after announcing a 5 billion yuan funding round and a new chairman: Yin Qi, former co-founder and CEO of Megvii, one of China’s first-generation AI unicorns. Yin also chairs Qianli Technology, Geely’s autonomous driving subsidiary—a connection that goes to the heart of StepFun’s commercial strategy.

A differentiation from peers, StepFun bets on AI embedded in hardware. Their models are deployed on over 42 million shipped devices, reaching approximately 20 million daily active users—with partners accounting for roughly 60% of China’s leading smartphone brands, including OPPO and Honor. The business model is closer to ARM by charing licensing fees and revenue-sharing from device manufacturers.

On the automotive side, StepFun and Geely jointly developed Agent OS, an intelligent cockpit system integrating StepFun’s multimodal and voice models, explicitly positioned as a Chinese answer to Tesla’s in-car Grok. StepFun’s target is one million vehicle integrations by end of 2026.

The investor lineup of the funding round includes Huaqin and Longcheer, both of which are top global phone ODM manufacturers; OmniVision is an image sensor supplier upstream in the smartphone camera supply chain; ZTE has already deployed StepFun models in its Nubia Z80 Ultra.

StepFun has also dismantled its red-chip (VIE) structure and converted to a joint-stock company—the corporate form required for a Hong Kong H-share listing. The target is to file in Hong Kong before June 30, with listing expected by year-end. The Hong Kong Investment Corporation, the city’s sovereign fund, is reportedly among the pre-IPO investors—making StepFun its sole large model bet.

Why now

In my view, the recent funding craze has two catalysts.

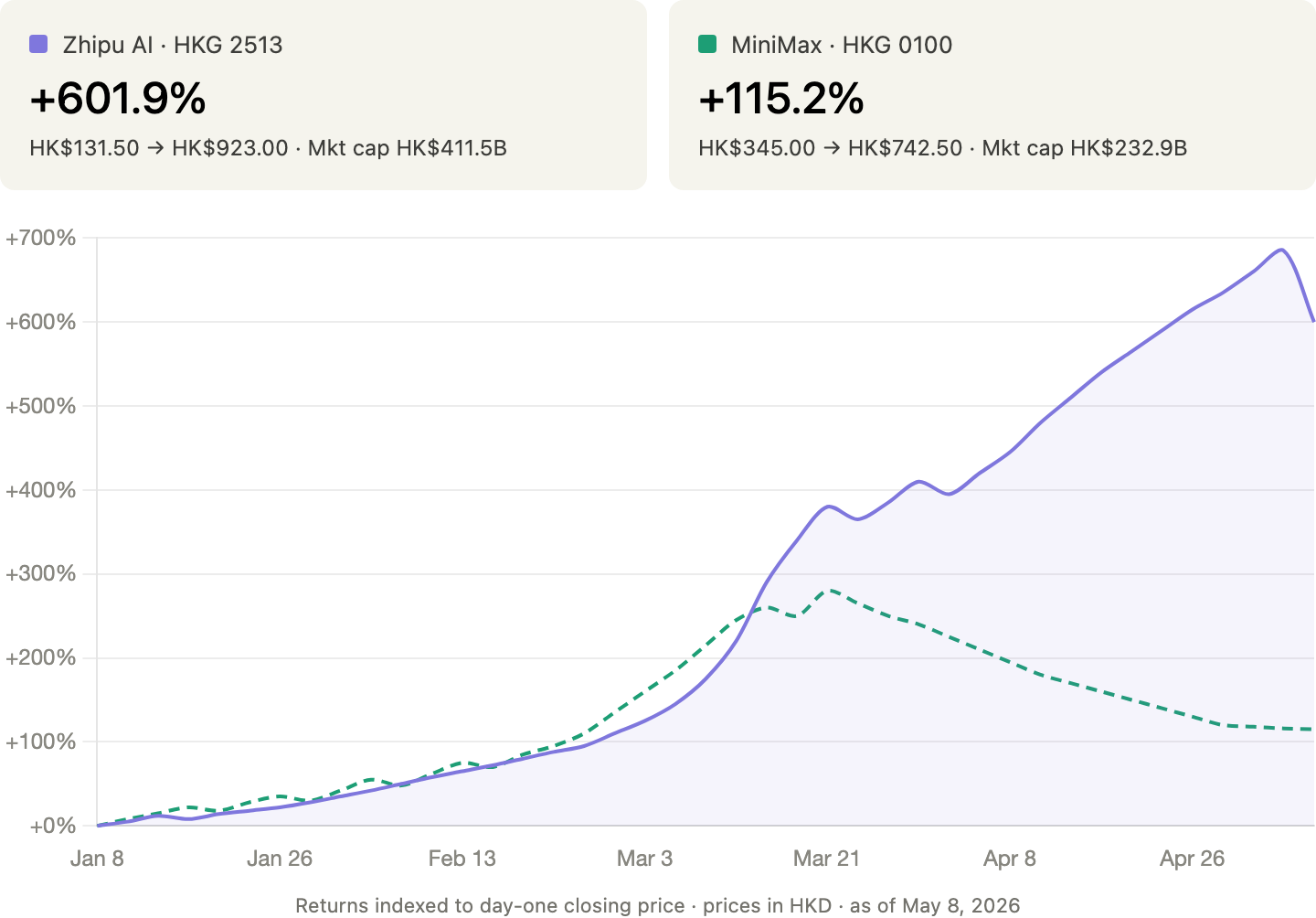

The first is the successful IPOs of Zhipu AI and MiniMax. Between 2020 and 2025, Chinese AI startups faced a structural exit problem. US Nasdaq—once the default destination for Chinese tech listings—became increasingly difficult due to deteriorating geopolitics and valuation discounts driven by perceived regulatory risk. At the same time, China’s anti-monopoly regulation made it harder for domestic tech giants to acquire startups. With no clear exit, Chinese VCs grew more risk-averse.

Then Hong Kong plays an important role. The exchange’s average daily turnover (ADT) hit HK$249.8 billion ($32 billion) in 2025—a 90% jump year-over-year. Its liquidity continues to show robust growth in early 2026, with Q1 ADT reaching HK$276.7 billion ($35 billion), a 14% year-on-year increase. IPO equity funds raised on the Main Board reached HK$285.8 billion ($36.5 billion) in 2025, a 225% increase from 2024.

Into this market walked Zhipu AI and MiniMax in January 2026—and they gave every private AI investor a benchmark. Zhipu has surged over 600% since its listing, reaching a market cap of roughly $56 billion. MiniMax doubled on its debut day and has since climbed to over $33 billion. Two companies that raised a combined $1.2 billion in their IPOs are now worth multiples of that.

The second catalyst is commercial. These companies have figured out how to make money by pushing the limits of model capabilities. Coding agents and agentic AI can now handle complex, multi-step tasks autonomously. White-collar employees, developers, and entrepreneurs are willing to pay for tokens at scale. This is visible in Moonshot’s ARR trajectory and in Zhipu’s model-as-a-service revenue growth.

This moment is reminiscent of 2023, when ChatGPT’s release in November 2022 sent Chinese VCs racing to incubate the country’s own OpenAI. The companies became unicorns quickly, then investment lines flatlined as questions mounted about their ability to commercialize. In late 2025, Claude Code, OpenClaw, and the broader agentic wave is another ChatGPT-like moment. Chinese AI companies responded by investing heavily in LLM agentic and coding capabilities, and their ARR grew exponentially.

To be clear, all of this is still small against the spending of China’s tech giants. Alibaba committed $53 billion over three years (2025–2028). ByteDance has boosted its AI infrastructure capex this year to more than 200 billion yuan ($30 billion).

A closing thought

I recently read Nathan Lambert’s notes from his visits to Chinese AI labs. One line stuck with me:

In China, the LLM community feels far more like an ecosystem than battling tribes. Across many off the record conversations, it’s nothing but respect for peers. All of the Chinese labs fear Bytedance with their popular Doubao model, which is the only frontier closed lab in China. At the same time, all of the labs have massive respect for DeepSeek as the lab with the best research taste in execution. When you meet with lab members off the record in the States, sparks fly quickly.

The most striking part of the humility of Chinese researchers is how they also often shrug on the business side, saying it’s not their problem, where everyone in the U.S. seems to be obsessed with various ecosystem-level industrial trends, from data sellers to compute or fundraising.

I have no doubt that in the near term, Chinese AI labs will continue this open and collaborative mindset. The market is large enough that aggressive internal competition isn’t yet necessary. Learning from each other through open releases is still the fastest way to improve. Ecosystem growth benefits everyone.

But as these companies continue to scale API revenue, bear increasingly high valuations, and face mounting commercialization pressure, the question is how long this friendly ecosystem can hold. At some point, open collaboration becomes competitive intelligence. When cut-throat competition arrives among Chinese AI labs—and it will—it will be just a matter of timing.

Until then, congratulations to all these companies that have overcome challenges and doubts to get here. The payday is well deserved.

The Big Fund entering DeepSeek's round is the structural signal here. This isn't just a unicorn funding wave — it's Beijing deciding that frontier AI R&D is strategic infrastructure, the same designation it gave SMIC in the 2010s.\n\nThe equity structure matters: Big Fund entry plus Liang Wenfeng's locked shares effectively nationalizes upside while keeping R&D risk private. Under this model, DeepSeek doesn't need strong commercial revenue — it needs to survive as a talent and compute node at the frontier. That's a governance structure Western AI investors don't have a framework for.\n\nSame week the Big Fund closed the .9B SMIC North acquisition, consolidating SMIC's flagship domestic fab into a wholly-owned subsidiary. Same institution, same week, same logic: designate as core infrastructure, fund it, own it domestically. DeepSeek just got the same designation SMIC got a decade ago. Worth watching what that pattern produces.

Crazy that a quant firm that turned into an AI company would value themselves at $10B when Z AI is trading publicly for 4x that